Auto loans in the UAE: How they work and a free EMI calculator to help you plan

Buying a car in the UAE can make everyday life easier, but it is also a big financial commitment. An auto loan lets you spread the cost over monthly installments so you don’t have to pay the full amount upfront.

Ready to compare your options, understand what fits your budget, and secure a sweet auto loan deal? You’re in the right place. Here, we’ll explain how auto loans work in the UAE, what affects monthly installments, how to use a car loan calculator, and what to check before applying.

We’ve partnered with leading financial institutions to help you find great car loan offers in the UAE. If needed, you can also use Daleel to find UAE mortgage deals and assess car or personal loan offers in Bahrain. Our focus is on providing you with the best deals, every time.

What is an auto loan?

An auto loan is money you borrow from a bank or lender to buy a car. You don't pay the full price upfront. Rather, the lender pays most of the cost, and you repay it in monthly installments over an agreed period.

You can get an auto loan to purchase a new or used vehicle, depending on the lender’s requirements as well as the car’s age, value, and condition. Your monthly payment usually depends on the car price, down payment, loan amount, interest or profit rate, and repayment tenure.

How do auto loans work in the UAE?

Auto loans in the UAE usually follow a simple process. First, you choose the car you want to buy. Next, you apply for financing through a bank or lender. And lastly, the lender reviews your income, documents, credit profile, and the vehicle details — before deciding whether to approve the loan.

If you get approval, you’ll need to pay the required down payment while the lender finances the remaining amount. You then repay the loan in monthly installments over the agreed tenure.

Once you understand the process, the next step is to check whether the repayment fits your monthly budget.

Auto loan eligibility requirements in the UAE

Auto loan eligibility in the UAE depends on the lender and the level of risk they’re willing to take, but most banks ask for a few key qualifications before approving your application. These requirements include:

- UAE residency

- A valid Emirates ID and residence visa

- The minimum age set by the bank

- A regular monthly income

- Salaried or self-employed status

- A stable employment or business history

- A credit profile that shows you can manage repayments

Lenders may also review your existing debts, salary transfer status, and the type of car you want to finance. The stronger your income and repayment history, the better your chances of getting approved on suitable terms.

Documents usually required for a car loan

Before approving a car loan, banks need to confirm your identity, income, residency status, and the details of the car you want to buy. The exact list may be different depending on the lender, but in most cases, the documents you will need are your:

- Emirates ID

- Passport copy

- UAE residence visa (if you’re an expat)

- Salary certificate or proof of income

- Recent bank statements

- Valid driving licence

- Car quotation, pro forma invoice, or vehicle valuation

If you are self-employed, the bank may ask for additional documents, such as trade license details or business bank statements. So to avoid delays, check the lender’s full list of required documents before applying.

After checking your eligibility and documents, the next step is understanding what affects the cost of the loan.

Key auto loan factors to keep in mind

When choosing an auto loan, don’t focus only on the monthly installment. A lower payment may look better at first, but the real cost also depends on the loan amount, interest rate, fees, insurance, and more.

- Loan amount: The amount you borrow after your down payment. The higher the loan amount, the higher your monthly installment is likely to be.

- Down payment: Most car loans require you to pay part of the car’s price upfront. A larger down payment can reduce how much you need to borrow.

- Repayment tenure: This is the period during which you must repay the loan. A longer repayment term can lower your monthly installment, but it may increase the total interest paid.

- Interest or profit rate: This affects both your monthly payment and the total cost of the loan. Some banks, including Emirates NBD, may offer different rates depending on your profile, salary transfer status, and the car you want to finance.

- Processing fees: Banks may charge a fee to process your application, so include this when comparing offers.

- Insurance: Comprehensive insurance is usually required when a car is financed. This can affect your total monthly cost.

- Early settlement: If you want to repay the loan early, check whether an early settlement fee applies.

New car loans vs used car loans

You can get financing for both new and used cars in the UAE, but the loan terms usually differ.

- New car loans: For new cars, the process is often more straightforward because the vehicle's value is clear and it has no prior ownership history. Banks may also offer longer repayment periods or more flexible terms, depending on your eligibility.

- Used car loans: The bank may need to check the car’s age, mileage, condition, and market value before approving the loan. Some lenders may also set limits on how old the car can be by the end of the loan tenure.

Many banks, like Emirates NBD, offer financing for both new and pre-owned cars, subject to the customer’s eligibility and the vehicle meeting the bank’s criteria. Before choosing either option, compare the total cost, monthly installment, insurance, and any extra fees.

Conventional auto loan vs Shariah-compliant auto financing

UAE residents can either opt for conventional auto loans or Islamic auto financing. While each option has a different monthly payment structure, they both help you buy a vehicle without paying the full amount out of pocket..

- Conventional auto loan: With a conventional auto loan, the bank lends you money to buy the car, and you repay the amount with interest over the agreed tenure. Here, your monthly installment depends on the loan amount, interest rate, and repayment period.

- Shariah-compliant auto loan: This type of car financing works best for Muslim customers who live by Shariah principles. Rather than charge interest, the bank may buy the car and sell it to you at an agreed profit, or use another approved finance structure. You still make regular payments, but the agreement is not interest-based.

Before making a decision, compare the monthly installment, total repayment amount, fees, and early settlement terms. But most importantly, ensure the structure aligns with your personal or religious preferences. For example, ENBD offers both regular loans and Islamic financing options (e.g., Ijarah).

How to apply for an auto loan in the UAE

Applying for an auto loan in the UAE is usually straightforward if you plan ahead. It typically involves the following steps:

- Define your vehicle budget.

- Choose the new or used car you want to buy.

- Check the bank’s eligibility requirements.

- Prepare your documents accordingly.

- Submit your loan application form.

- Wait for the bank’s approval and vehicle checks (if needed).

- Review the final offer, including the rate, tenure, fees, and insurance requirements.

- Make the down payment and complete the purchase.

Note: Don’t be in a hurry to sign. Ensure you confirm the total repayment amount due, not just the monthly installment, because that’s what shows you what the car will really cost over time.

How can a car loan calculator help you plan?

A car loan calculator gives you a clear idea of what your monthly payments could look like before committing to the loan. Instead of guessing whether a car fits your budget, you can enter the car price, down payment, loan tenure, and expected rate to see an estimate of your potential monthly installment.

With an auto loan calculator, you can also test different scenarios. For example, you can check how your monthly payment changes if you increase your down payment, choose a shorter or longer tenure, or compare different loan amounts. After testing and estimating, you’ll be in a better position to decide on an auto financing option.

Free car loan calculator

A range of car loan calculators exist, but to streamline your search, we’ve narrowed it down to one. So whether you’re just weighing your options for the future or want to buy a car as soon as possible, try the Emirates NBD auto cash loan calculator.

The Emirates NBD auto loan calculator provides a useful estimate before you apply, letting you calculate your EMI for up to 60 months. However, it does not guarantee loan approval or the final rate.

Meanwhile, loan benefits and rates are still dependent on your banking segment, eligibility, and borrowing capacity, in line with the bank’s terms and conditions (as well as Central Bank regulations).

How to use a car loan calculator

Once you have your basic numbers ready, using a car loan calculator should only take a few minutes. Unsure where to start? Follow these three steps:

Step 1: Gather your figures

Before you open the calculator, write down the key details you need:

- The on-road car price.

- Your planned down payment.

- Your preferred loan term.

- The interest or profit rate you have been quoted.

- Any insurance costs or fees.

Taking note of these figures can make it easier to test the same numbers across different calculators or loan offers.

Step 2: Enter the details in the calculator

Start with simple numbers to get a baseline. For example, you could enter an AED 100,000 car price or loan amount, along with a 48-month repayment term.

Once you see the first estimated monthly installment, feel free to adjust the inputs to match your actual quote. If the calculator includes an insurance or down payment field, add those too. Skipping insurance or fees can make the monthly cost look lower than it really is. Either way, you’ll get more details after speaking with a representative from the lender.

Note: Try at least two different loan tenures. A longer term may reduce the monthly installment, while a shorter term may lower the total interest you pay.

Step 3: Review the EMI breakdown

After the calculator gives you an estimated monthly installment (EMI), check whether it fits your monthly budget. In the UAE, banks usually consider your debt-to-income ratio (DBR), so your total monthly debt repayments should stay within the 50% DBR limit.

Say your salary is AED 10,000. Your existing loan repayments (e.g., from credit card debt) plus the new car installment should stay below AED 5,000 per month. Also check the total interest, final payoff date, and any extra costs included in the calculator’s result.

Take a screenshot or save the results while comparing offers from different lenders. This step lets you go back to see which option is actually more affordable in the long run, not just which one has the lowest monthly payment.

Understanding your auto loan calculator results

As soon as the calculator gives you a result, do not stop at the monthly payment. The installment matters, but it is only one part of the full cost. You also need to look at the total interest, repayment structure, and how the numbers change when you adjust the rate, tenure, or down payment. Not all calculators will show you these details, but pay attention if yours does.

What your monthly payment means (plus how it is calculated)

Your monthly installment is the amount you pay every month until the loan is cleared. But lenders calculate that payment differently depending on your loan type.

With a reducing balance loan, you only pay interest on the amount you still owe per month. This means your early payments usually include more interest, while later payments go more toward reducing the loan balance.

With a flat-rate loan, lenders calculate interest on the original loan amount for the full term. This calculation can make the rate look lower, but ensure you estimate how much you will pay in total, especially if you plan to settle the loan early. It isn’t always the more cost-effective option.

Total interest charged

The total interest shows how much the loan will cost you beyond the amount borrowed. For a flat-rate loan, the calculation is:

Total interest = Principal × Flat rate × Years

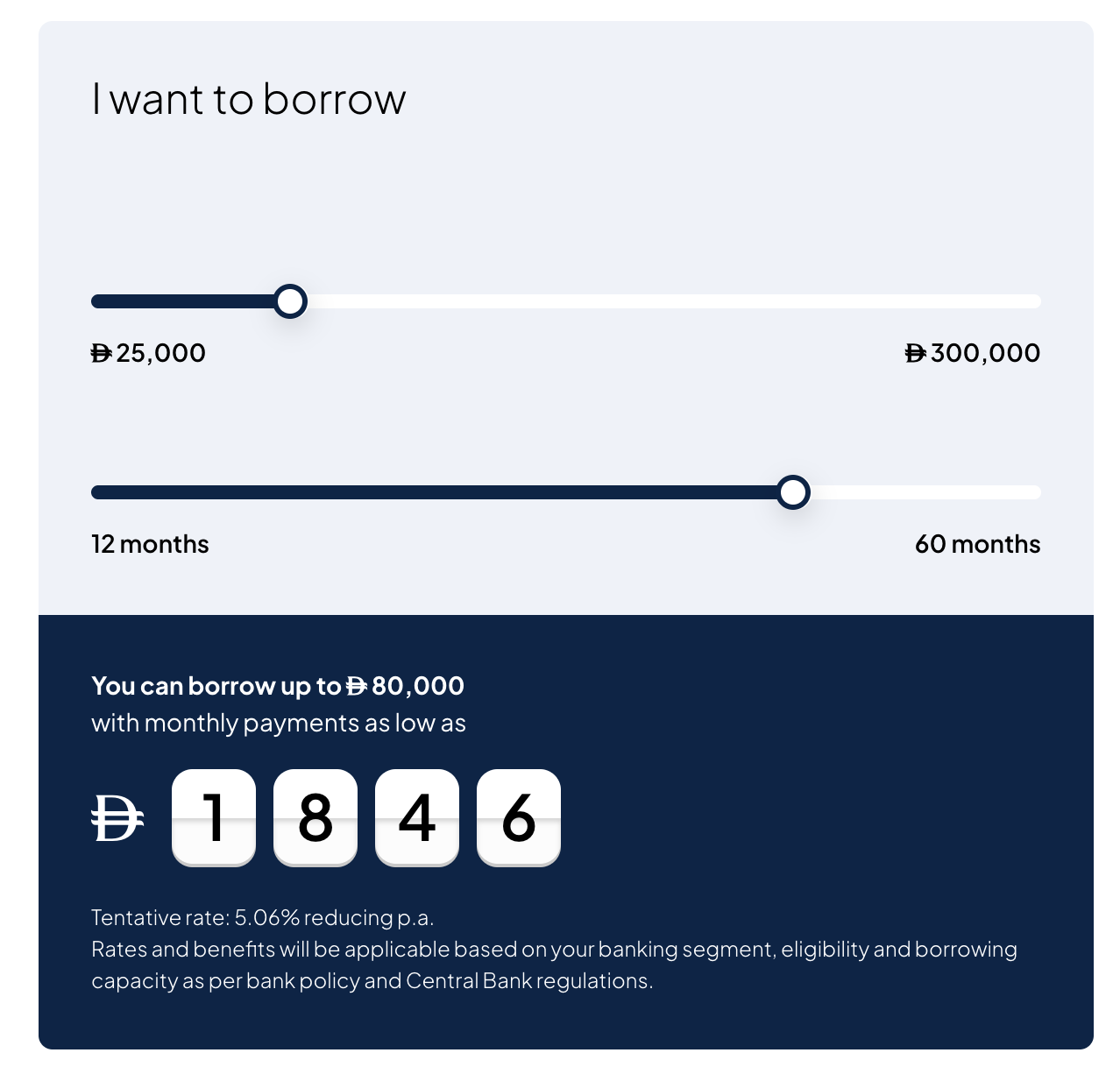

For example, on an AED 80,000 loan at Emirates NBD’s 2.69% flat rate over five years, the total interest adds up to about AED 10,760.

AED 80,000 x 2.69% x 5 = AED 10,760

You may also see the same loan expressed as an equivalent reducing rate. In this example, the equivalent reducing rate is 5.06% p.a., which produces the same total cost but looks higher on the surface. Our take? Always compare loan offers using the reducing rate; they show the true annual cost of borrowing compared to fixed rates.

Amortization schedule overview

An amortization schedule shows how each monthly payment is split between interest and principal. In a reducing-rate loan, the interest portion usually decreases over time as the outstanding balance declines, while the principal portion increases.

Some calculators let you export this schedule to a spreadsheet. This can be useful if you want to see when more of your payment starts going toward the car loan balance instead of interest.

Comparing car loan interest rates in the UAE

After estimating your EMI, the next step is to see how different interest rates affect that number. A small difference in rate can change your monthly payment and the total amount you repay, so it‘s good to assess offers carefully before choosing a lender.

Flat vs reducing rates

Car loan rates in the UAE are usually shown as either flat rates or reducing rates.

A flat rate is calculated on the original loan amount for the full tenure. A reducing rate is calculated on the balance you still owe, so the interest portion reduces as you repay the loan.

Flat rates usually look lower, which is why they are often used in advertisements. To compare two offers fairly and choose the best one, ask the lender for both the flat rate and the reducing rate. As a rough guide, a 2.5% flat rate can be equal to a reducing rate of around 4.7% to 5.0%, depending on the loan term.

Once you have the reducing rate, enter it into your calculator to get a clearer idea of the actual EMI.

Bank promotions and offers

Banks in the UAE sometimes offer limited-time promotions like reduced rates, waived processing fees, or lower insurance costs. These can be helpful, but check the details and fine print as well; don’t only focus on the headline rate.

Ask the bank these questions:

- Does the promoted rate require salary transfer?

- Does the rate apply for the full loan term or only the first few months?

Some banks give better rates to customers who transfer their salary. To see the real difference, enter both the salary transfer rate and the non-transfer rate into the calculator and compare the monthly EMI side by side.

Online comparison tools

Online comparison platforms like Daleel can help you see loan rates from different lenders in one place. Use them to shortlist competitive offers, then enter each rate into your own calculator.

This gives you a fairer comparison because every offer is tested against your actual loan amount, down payment, and preferred tenure, rather than a generic example.

Smart ways to lower your monthly payments

If the EMI from the calculator is higher than you expected, do not treat it as the final number. A few changes can bring the monthly cost down or reduce how much you pay overall.

Pay a larger down payment

A bigger down payment reduces the amount you need to finance. For example, increasing your deposit from 20% to 30% on an AED 200,000 car brings the financed amount down from AED 160,000 to AED 140,000.

At Emirates NBD’s published flat rate of 2.69% per annum, that lower loan amount can reduce your monthly installment and save you several thousand dirhams in total interest over the life of the loan.

Shorten the loan tenure

A shorter loan term can increase your monthly installment, but it usually lowers the total interest you pay over time. For example, on an AED 80,000 loan at 2.69% flat, a 60-month term generates AED 10,760 in total interest.

If you reduce the term to 48 months, the total interest drops to AED 8,608. That is a saving of AED 2,152. Try both options in the calculator to find the point where your monthly cash flow and total interest cost align.

Negotiate insurance costs

Comprehensive insurance is usually required while your car is under finance, but you do not always have to buy it through your lender. Make sure to compare quotes from external insurers before you decide.

If the calculator has an insurance field, enter the lower premium and check how much it changes your total monthly cost. Even AED 200 in monthly savings on insurance adds up to AED 12,000 over five years. Review the policy every year as well, so you can renegotiate at renewal rather than automatically accept the same price.

Refinance or settle early

If you already have a car loan and later find a better rate, refinancing or early settlement may help you save money. Under Central Bank of the UAE (CBUAE) regulations, the early settlement fee is capped at 1% of the outstanding loan balance or AED 10,000, whichever is lower.

To check whether car loan refinancing makes sense:

- Enter your current outstanding balance as the new loan amount in the calculator.

- Add the lower rate you have been offered.

- Compare the new total cost against your remaining payments.

If the savings exceed the settlement fee, the numbers may support switching.

Choose a loan that fits your budget and needs

A car loan can make buying a car more manageable, but it should still fit comfortably into your monthly budget. Use the calculator to test different repayment options, compare the full cost, and avoid choosing a loan based only on the lowest installment.

But if you are looking for other financing options in the UAE, e.g., home loans, use Daleel to review available options and take your pick.

Join Daleel today to get started.